Introduction

The United States has long pinned hopes on automation, particularly “lights-out factories” (fully automated factories), to drive manufacturing reshoring, aiming to replace human labor with robots and smart systems to cut costs and boost competitiveness. However, reality falls far short of this vision. In 2025, despite 5G covering 88% of North America’s population, poor signal quality, high deployment costs, and community resistance to base station construction make lights-out factories nearly unfeasible in the U.S. Compounding this, industrial robot supply chains face sanctions and tariffs, inflating procurement costs and making unmanned factories far pricier than traditional manned factories. This report reexamines the issue, analyzing technical prerequisites, industrial gaps, cost comparisons, and policy dilemmas to argue that the U.S. must pivot to government-led infrastructure investment to revive manufacturing.

5G Networks: Technical Barriers and U.S. Deployment Challenges

Lights-out factories rely on real-time, ultra-reliable communication networks, with only 5G meeting the demands for low latency (<1ms), high bandwidth, and stability. Fiber optics are impractical due to complex wiring (prone to damage from bending), WiFi has limited coverage, and 4G lacks sufficient speed, rendering these alternatives unsuitable for fully automated production lines.

However, U.S. 5G adoption faces multiple hurdles. As of Q1 2025, North America has 314 million 5G connections, but actual adoption is only 25% in urban areas and 10% in rural industrial zones, with many areas still reliant on unstable 4G (LTE). Deployment challenges stem from cultural and institutional resistance: affluent communities frequently file lawsuits or protest against base stations, citing health concerns from “radiation” (NIMBYism), delaying approvals by months or years.

Moreover, access costs are steep—a typical U.S. household pays over $150/month for a three-line 5G plan, 3-5 times higher than China’s average. Bureaucratic red tape further complicates matters, with local permitting processes stalling broadband projects. Political interference, such as Representative Alexandria Ocasio-Cortez’s public opposition to Amazon’s second headquarters (HQ2) in New York, which led to its cancellation, exemplifies similar resistance to base stations and power plants, hindering industrial automation.

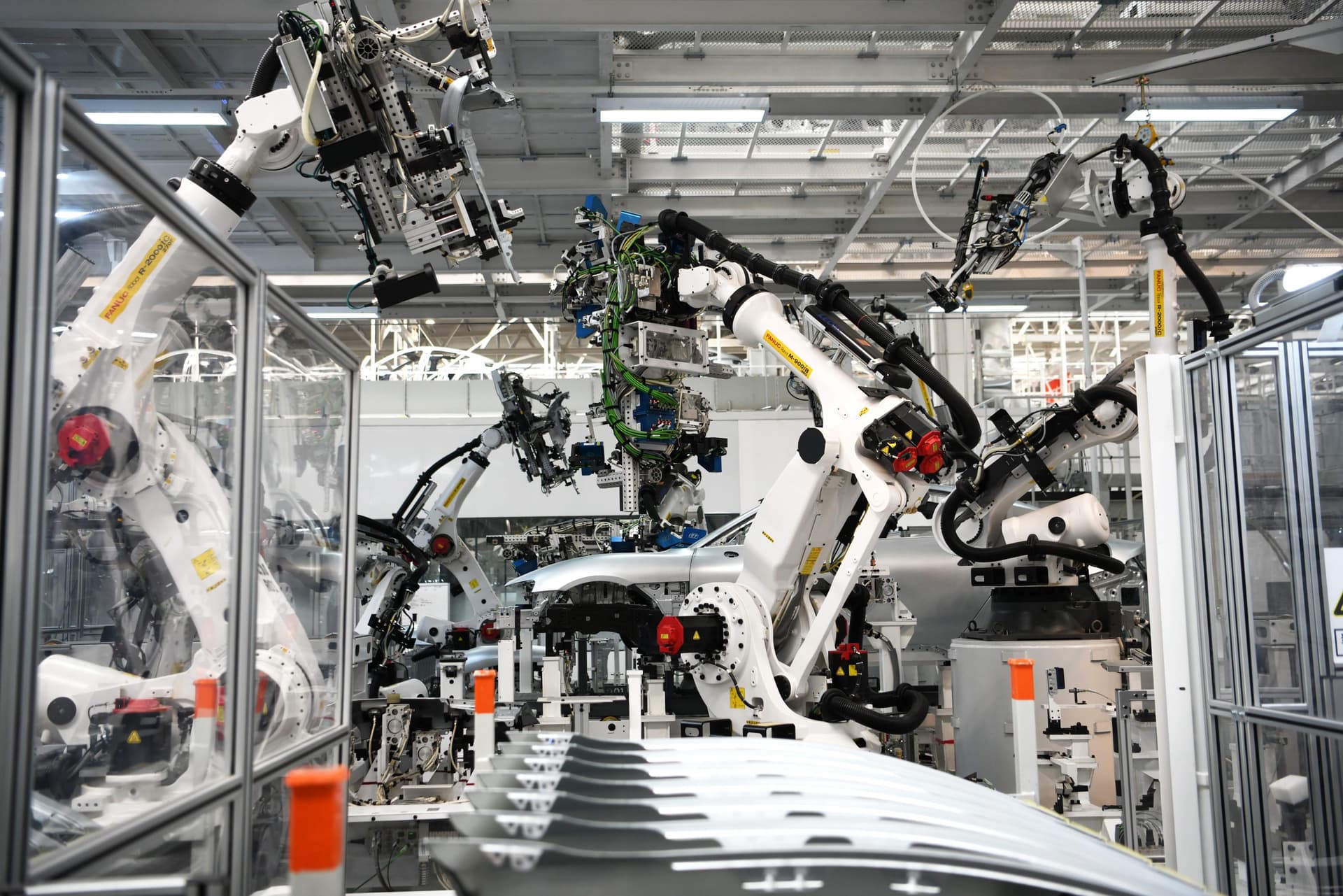

Industrial Robotics: U.S. Gaps and Global Shifts

The U.S. lacks major domestic players in industrial robotics. Companies like Boston Dynamics and Tesla (with its Optimus project) focus on complex humanoid robots for general tasks, aiming to fully replace humans rather than optimizing industrial arms for tasks like welding or assembly. Boston Dynamics’ Atlas emphasizes dynamic mobility, while Optimus targets scalability, but neither has scaled to factory production, often serving more as capital market hype than practical solutions.

Globally, the industrial robotics market is led by the “Big Four”: Switzerland/Sweden’s ABB, Germany’s KUKA, and Japan’s Fanuc and Yaskawa. In 2023, ABB and Japan’s Epson each held 13% market share. Chinese firms like SIASUN and Estun Automation are rapidly gaining ground, with Estun capturing 9.5% of the market. China dominates smart manufacturing: in 2025, it accounts for over 40% (roughly 80) of the World Economic Forum’s 201 global Lighthouse factories, the gold standard for Industry 4.0. In 2024, global industrial robot installations reached 542,000 units, with China absorbing 54% (295,000 units) and operating a stockpile of over 2 million units.

U.S. policies are contradictory: to curb China, companies like SIASUN face Entity List sanctions and “1260H” military-civil fusion bans, blocking high-tech component sales. Meanwhile, Trump’s 2025 tariffs (15%-39%) on robots from Japan, Germany, and Switzerland inflate procurement costs 3-5 times. Ironically, KUKA, now owned by China’s Midea Group, risks further sanctions, potentially leaving the U.S. without a reliable robot supply chain.

| Metric | Global | China | U.S. |

|---|---|---|---|

| 2024 Installations (Units) | 542,000 | 295,000 (54%) | <10,000 (Domestic) |

| Lighthouse Factories (2025) | 201 | ~80 (40%) | 5 |

| Major Firms’ Market Share | ABB/Epson: 13% | Estun: 9.5% | No Domestic Leaders |

Cost Analysis: The Practical Edge of Manned Factories

Lights-out factories sound efficient but carry exorbitant hidden costs in the U.S. 5G infrastructure costs are 8-10 times higher than China’s (millions per tower), and robot procurement from Europe/Japan is 3-5 times pricier post-tariffs. Energy demands are massive: a rare-earth refining lights-out factory may require nuclear plant-level power, yet building nuclear or coal plants faces community backlash. Transportation infrastructure is equally daunting—factories must self-fund road connections, costing hundreds of millions per site.

In contrast, manned factories are more economical. Even with U.S. worker salaries at $100,000/year (10 times China’s rural wages of $10,000), labor costs are only 20%-30% of total expenses, far below automation’s upfront costs (single robot arm: $50,000; full factory: $5M+) and maintenance fees. ROI for automation takes 3-5 years, extended to 10 years by infrastructure delays. In a labor-scarce but infrastructure-constrained nation, manned factories are more practical.

| Cost Item | Lights-Out Factory (U.S. Estimate) | Manned Factory (U.S. Estimate) |

|---|---|---|

| 5G/Network Infrastructure | 8-10x China ($100M+) | Not Required Fully |

| Robot Procurement | 3-5x China (Post-Tariffs) | Partial Automation, 50% Savings |

| Energy/Transport | Nuclear Plant + Roads ($1B+) | Existing Grid + Public Roads |

| Labor (Annual) | $0 | $100,000/Worker (Flexible) |

| Total Hidden Costs | High (Delay Risks) | Low (Immediate Operation) |

Government’s Role: From Free-Market Myth to National Capitalism

U.S. manufacturing reshoring requires abandoning the “free market” myth and embracing government-led national capitalism to provide public services like high-speed rail, 5G, power, and highways. Past efforts have faltered: from Obama to Trump to Biden’s $1 trillion infrastructure bill, progress is sluggish. For instance, Biden’s $7.5 billion EV charging investment yielded fewer than 400 ports by 2025, while China’s Huawei alone deploys more annually. Green energy firms rely on subsidies and collapse without them.

Solar power holds promise: rooftop panels on Midwestern homes could meet 80% of residential electricity needs, freeing power for industry and data centers, potentially aiding desertification control. Yet U.S. solar panels cost 31 cents/watt—7-10 times China’s—due to 145% tariffs. Lifting tariffs and offering subsidies could lower costs to 3-4 cents/watt, boosting adoption.

Conclusion

Lights-out factories are not the panacea for U.S. manufacturing reshoring; their high costs and infrastructure barriers render them a pipe dream. The government must invest $2 trillion in nationwide infrastructure (5G, power, transport) and adopt a “strong government” model to forge political consensus. Without this, manufacturing revival will remain elusive, and China will continue to lead the global smart manufacturing wave.