It has been nearly a year since the implementation of major economic policies aimed at revitalizing American industry. A core promise was to bring manufacturing back to the U.S. through measures like tariffs, presented as tools to attract or compel foreign investment. Official announcements have listed staggering investment commitments from global companies and nations, totaling in the trillions of dollars, suggesting a booming return of factories.

However, data tells a different story. According to reports tracking foreign “greenfield” investment—funds specifically for building new factories or expanding production—there has been no significant increase compared to the previous year. The actual investment flows fall far short of the grand totals publicized. Notably, a large portion of the limited new investment comes from a single semiconductor company, while investments from other major pledged partners like Japan and South Korea have not materialized as projected in this category. Furthermore, the number of new U.S. manufacturing projects has declined, not increased.

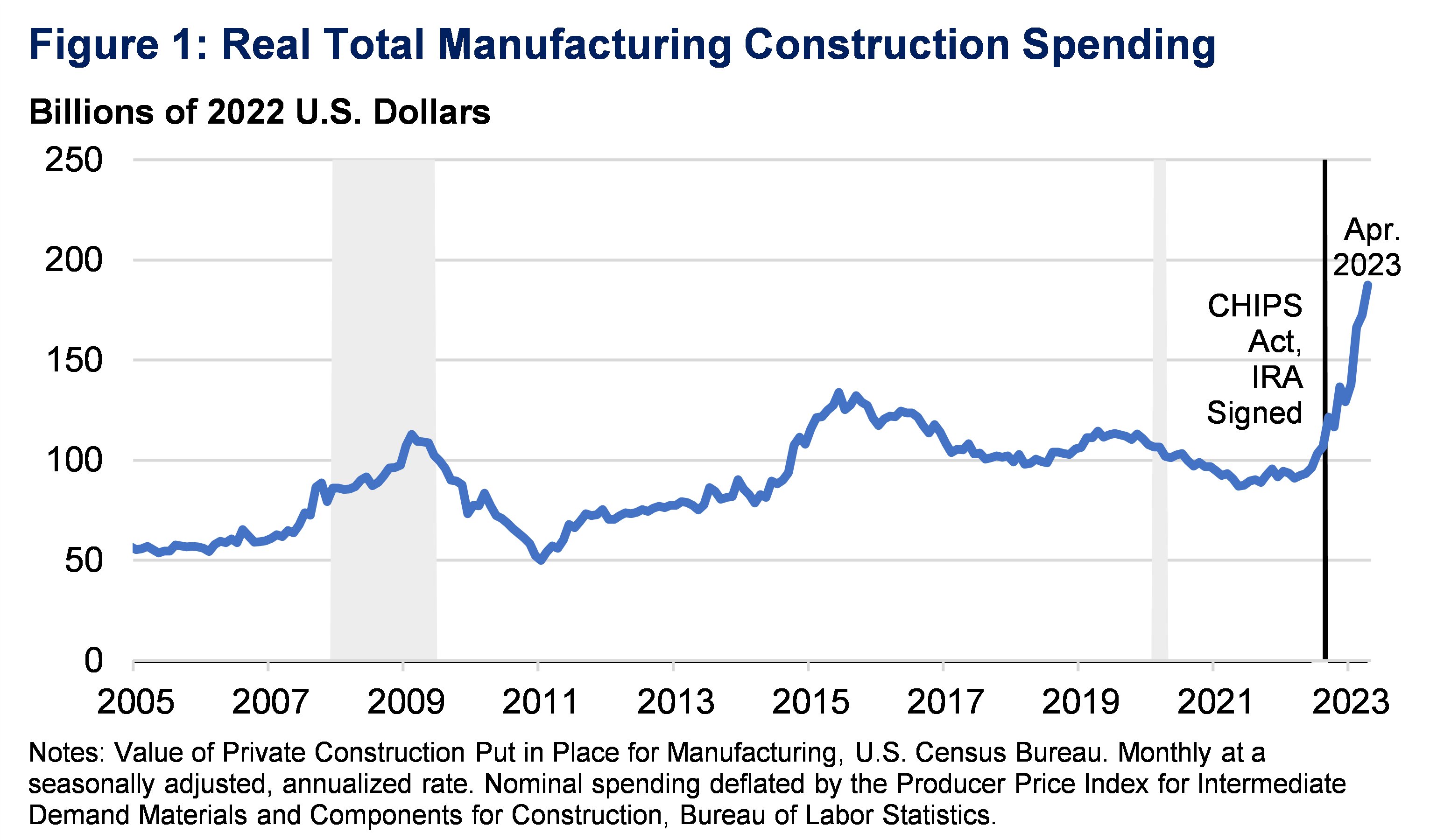

The argument that tariffs would spur a manufacturing revival isn’t supported by these investment figures, which show no correlation with tariff rates. Looking domestically, while there was a surge in factory construction in 2023-2024, this trend sharply reversed in 2025. Analysts attribute this to uncertainty and rising costs from tariffs, making projects financially unfeasible. More critically, the total number of manufacturing jobs has been consistently falling, losing hundreds of thousands of positions since the policy rollout. The job losses are concentrated in high-value sectors like semiconductors, automotive parts, and aerospace—precisely the industries meant to be pillars of a resurgence.

This points to a deeper issue: building factories is not the same as rebuilding a manufacturing ecosystem. True industrialization requires a complete supply chain network, not just final assembly plants. Without a deep supplier base, new U.S. factories risk becoming costly assembly centers dependent on imported parts, potentially increasing, not decreasing, reliance on foreign supply chains—particularly China. A case in point is the U.S. drone industry. Despite having political connections, massive defense contracts, and a lack of major competitors, some prominent American drone companies struggle. Investigations reveal many rely heavily on Chinese components for their products, with some merely “assembling” or “rebranding” imported kits. One highly-valued defense contractor’s drones have reportedly faced repeated operational failures in tests and real-world use, raising serious questions about capability versus marketing and lobbying prowess.

The recent relaxation of bans on using Chinese drone components for the U.S. military underscores this dependency. The narrative shifted from Chinese drones being an “unacceptable risk” to a necessary part of the supply chain within months. This reality contradicts simple economic models that suggest raising costs abroad through tariffs will automatically bring complex manufacturing home. The subsidies and investments often flow to companies skilled in navigating political channels rather than building foundational industrial capacity. The current approach may be creating expensive, inefficient assembly outposts rather than a genuine, competitive, and secure manufacturing renaissance.